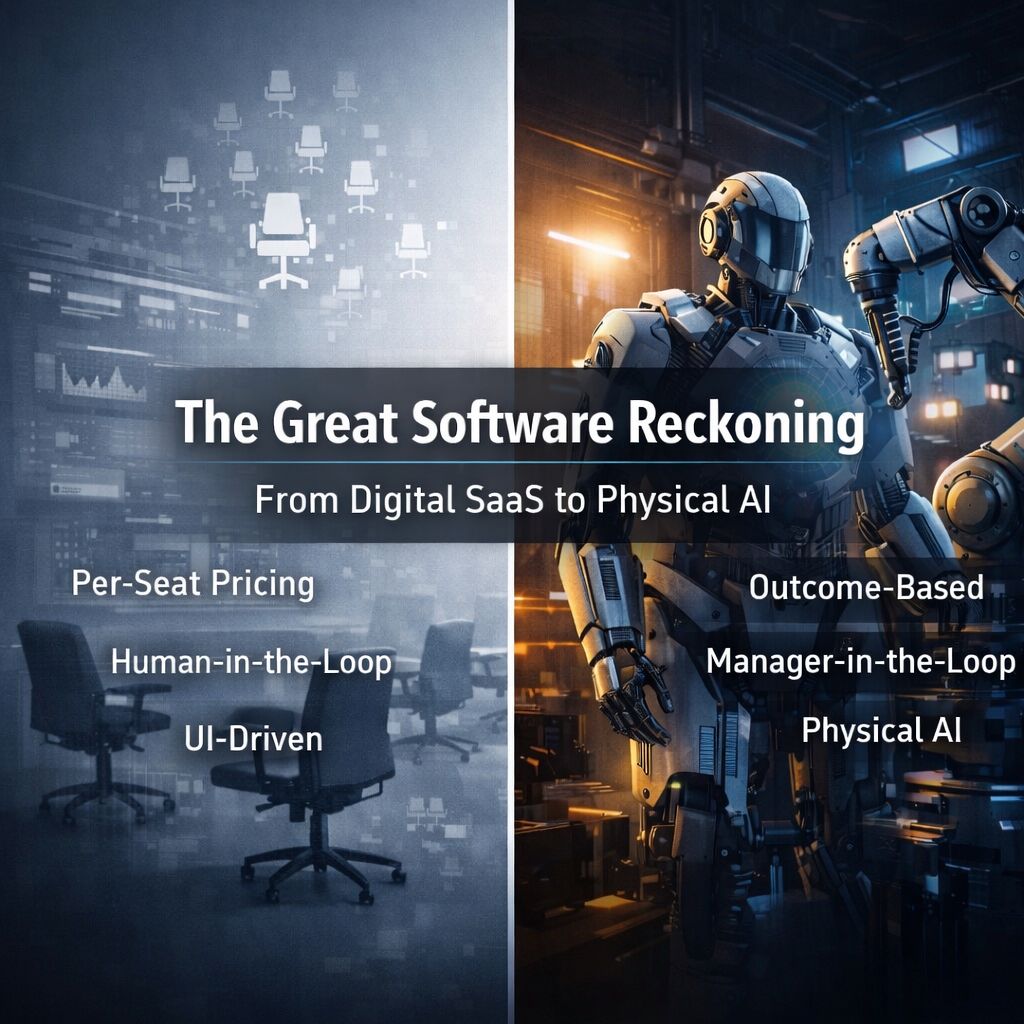

The enterprise technology landscape is currently undergoing its most seismic shift since the transition from on-premise servers to the cloud. For the modern investor, the traditional "SaaS" playbook—relying on seat-based licensing and horizontal workflow tools—is no longer a safe harbor. We are entering an era defined by the "Death of the Seat" and the "Rise of the Autonomous Outcome".

I. The Collapse of the Traditional SaaS Model

The "Software-as-a-Service" model is being dismantled by three primary forces that are fundamentally inverting the Silicon Valley business model:

- Agentic Displacement: As AI agents perform tasks previously handled by humans, the "per-seat" revenue model becomes a liability. If AI can do the work of five people, seat-based pricing leads to an 80% drop in software spend.

- UI Commoditization: Generative AI has made it trivial to create beautiful front-ends. Tools that are merely "wrappers" around LLMs lack defensive moats and are easily replicated via "vibe-coding" and natural language.

- Horizontal Compression: Generic tools (note-takers, basic CRMs) are being swallowed by Big Tech ecosystems that integrate AI at the operating system level.

II. The Technological Catalyst: Modern Agentic AI

Recent breakthroughs in model reasoning and multimodal interaction have shifted AI from a "feature" to "labor". We are moving from Human-in-the-loop to Manager-in-the-loop, where humans manage AI agents that execute the work.

Breakthroughs in Execution

- The Interface Shift (Computer Use): Modern agents can now view screens, move cursors, and type like humans. This allows them to navigate legacy ERPs and banking portals that lack modern APIs, turning any software into a backend for an AI agent.

- The Context Revolution: Standardized high-capacity context windows now allow agents to ingest entire codebases or a full year of legal logs in one pass. This destroys the value proposition of traditional "Knowledge Management" middleware.

- The Orchestration Shift (Agent Teams): High-level models now act as orchestration layers, breaking complex goals into sub-tasks and managing specialized sub-agents (e.g., researchers, coders, or QA). This directly threatens project management SaaS as the AI becomes the manager.

III. Sector-Specific Disruption & "Service-as-Software"

The market is shifting from selling tools to selling labor and liability. This model, "Service-as-Software," captures value by delivering finished outcomes rather than mere "labor-saving" features.

- CRM (The "Empty Chair" Crisis): Visual dashboards are becoming irrelevant as AI agents use "Computer Use" to research and update records directly. Value shifts to Data Gravity—owning the history agents need to act.

- FinOps & Agentic Commerce: Agents handle autonomous procurement via Agentic Wallets (virtual cards with budget limits). High-capacity context windows allow for zero-touch reconciliation and autonomous dispute resolution.

- Software "Autopilot": Engineering is moving beyond autocomplete to "Autopilot" execution, where agents autonomously resolve complex bug tickets across multiple files.

- Trust as a Product: As agents take high-stakes actions, the new moat is Liability. "Insured SaaS" providers who financially and legally guarantee agent outcomes will dominate the enterprise.

IV. The New Frontier: Physical AI

The most significant evolution in 2026 is Physical AI—the convergence of LLMs with the world of "atoms". While digital AI is becoming a commodity, Physical AI creates a massive hardware-software moat.

- VLA Models: Physical AI uses Vision-Language-Action (VLA) models to perceive, reason about, and interact with the 3D world.

- Physics-Aware: Unlike traditional robotics programmed for repetitive tasks, these systems adapt to unstructured environments and learn from tactile feedback.

- The Moat: Defensibility shifts from brand effects to Proprietary Physical Interaction Data and real-world telemetry.

V. Strategic Pivot for Investors: Multi-Vertical Applications

Investors must pivot from tools that assist humans to systems that bridge the gap between intelligence and execution.

- Healthcare & Life Sciences: Focus on autonomous lab automation, surgical robotics with active guardrails, and "Human-in-the-Loop" diagnostic systems.

- Science, Engineering, & Space (SET): Prioritize "Autonomous Orbital Operations" and hardware-native software managing edge-computing in harsh environments where human intervention is impossible.

- Industrial & Manufacturing: Target foundation models that manage robotic assembly and quality control to support the "re-shoring" movement.

- Finance & Professional Services: Invest in systems where agents handle autonomous procurement, dispute resolution, and reconciliation with minimal human oversight.

- Logistics & Supply Chain: Look for platforms solving complex logistics—such as in space-tech—where proprietary data loops create a defensive moat.

- Outcome-Based Moats: Prioritize "Insured SaaS" vendors who provide "Trust as a Product" by financially and legally guaranteeing the outcomes of their agents.

VI. Conclusion: The New Moats

The ultimate winners will be those who control the Data Gravity of the Physical World. In an era of autonomous agents, the winners will not be those who build better tools for humans, but those who build the digital and physical workforce itself.