Space is no longer the final frontier—it’s becoming the next foundational layer of global infrastructure. What began as a state-sponsored, capital-intensive arena is now a dynamic, commercially viable domain attracting startups, investors, and global collaboration. From launch vehicles to hyperspectral satellites and AI-powered earth analytics, we are entering a phase where space is not only accessible but essential to terrestrial innovation. This is especially true in India, where policy liberalization, engineering talent, and cost advantages are aligning to place the country at the center of the New Space era. At Inflexor Ventures, we believe the space opportunity is real, addressable, and full of defensible value creation.

Space technology has historically been dominated by government agencies, with missions primarily focused on national priorities—such as weather forecasting, communication, navigation, and defense. In India, this foundation was built by ISRO, which over decades developed the core capabilities of launch vehicles, satellite systems, and mission planning.

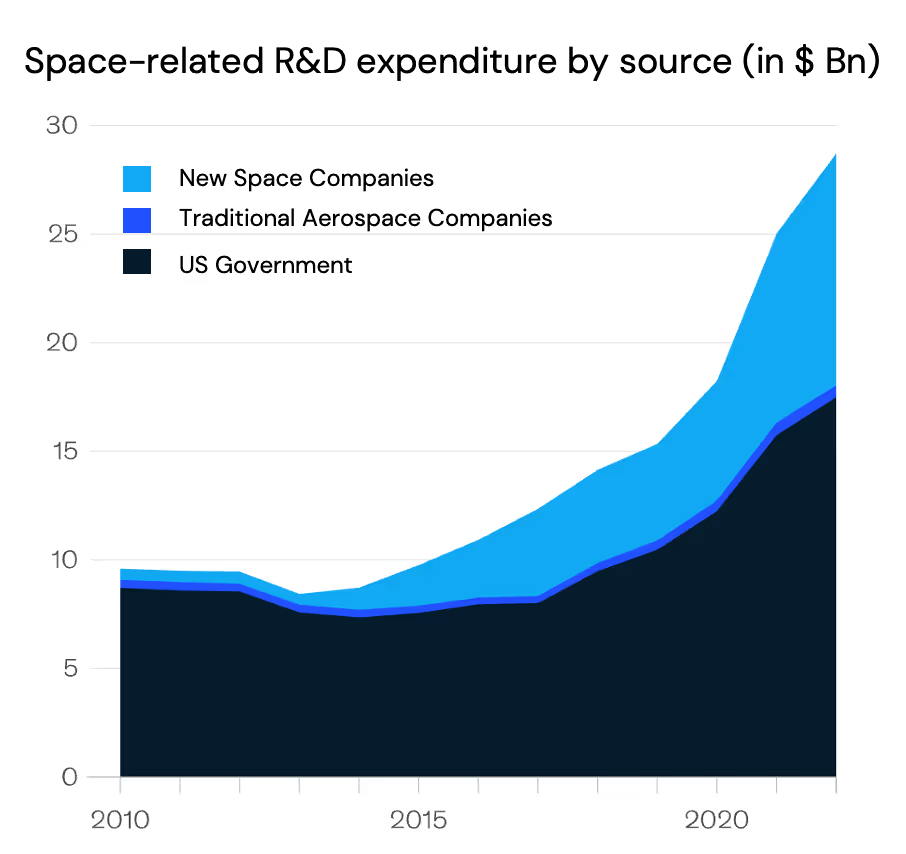

However, over the last few years, this dynamic has started to shift significantly. What was once a government-centric domain is now opening up to commercial participation across the value chain. Globally, private companies are driving an increasing share of investment and innovation in space-related technologies—from reusable rockets to miniaturized satellites and data-focused applications. This trend is also visible in India, where the government has created a more supportive regulatory framework to enable private sector growth.

Data from space-related R&D spending shows a marked rise in contributions from private enterprises and traditional aerospace firms, complementing ongoing public expenditure. This change signals not just the entry of new players, but a structural transformation in how space systems are conceived, developed, and deployed.

The result is a more modular, commercially viable, and scalable approach to space infrastructure. Private startups are now able to build upon decades of sovereign investment while bringing new agility, software capabilities, and user-oriented applications to market. This is the foundation of what many refer to as the “New Space” economy—a collaborative ecosystem where both public and private contributions accelerate overall progress.

Global launch activity has surged dramatically in recent years. According to the Space Foundation, 259 launches were completed in 2024, averaging one every 34 hours—up from 223 in 2023 and 186 in 2022. Of those, the Satellite Industry Association reports that 2,695 satellites and a total payload mass of 2,172 tons were delivered to orbit. As of the end of 2024, over 11,500 satellites were operational in space, a sharp increase from around 3,400 in 2020.

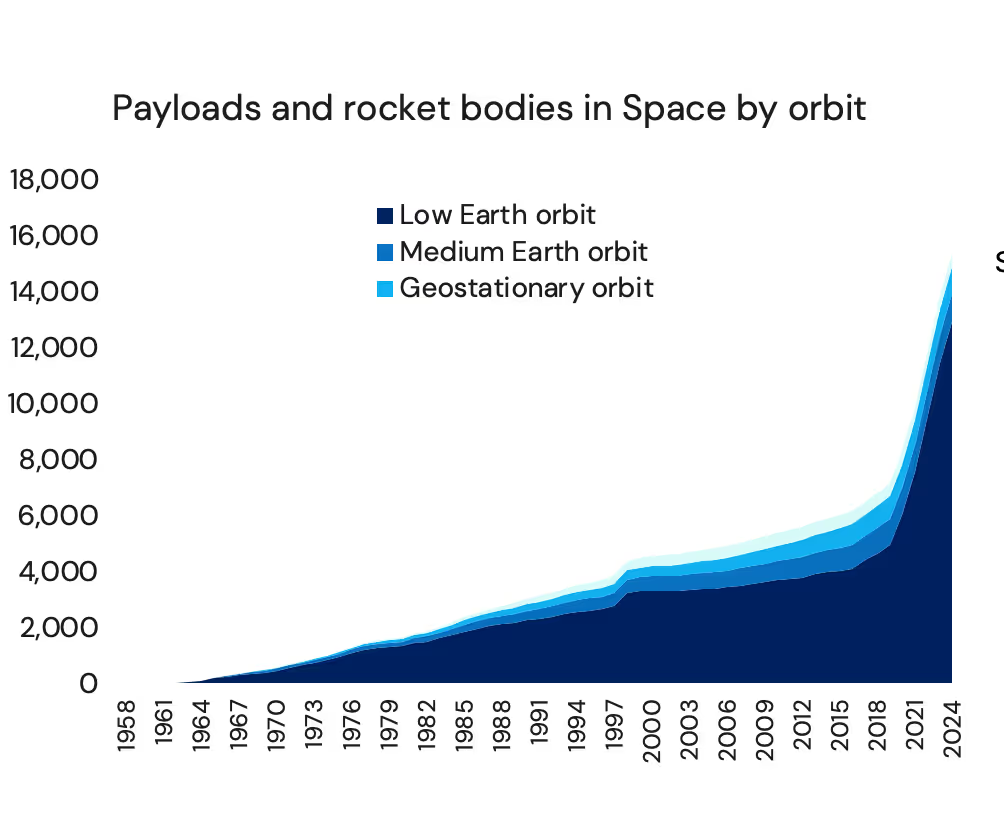

As of now since 1957, more than 20,000 objects have been launched into space up from around 10,000 objects in 2020.

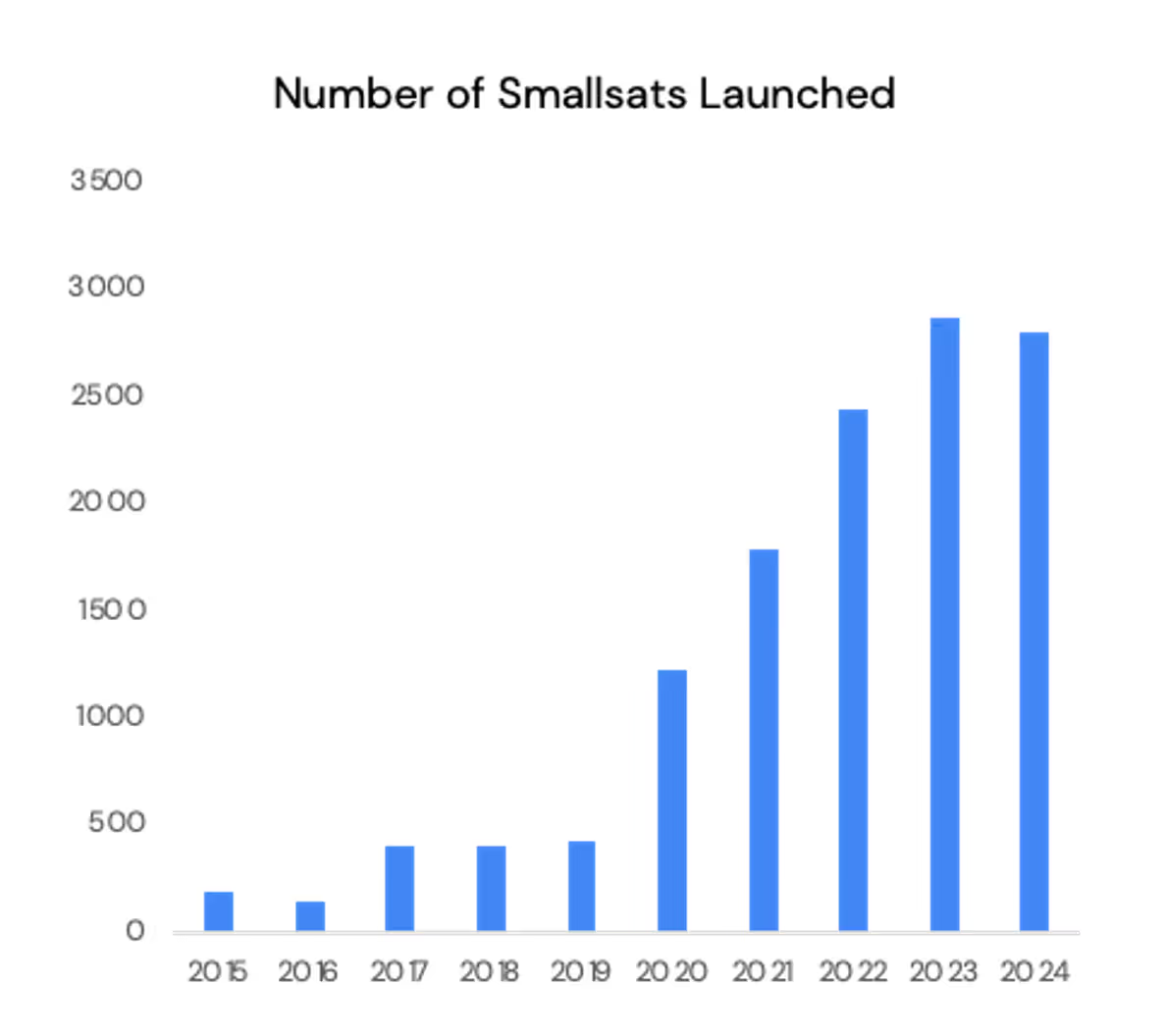

The global space economy is entering a high-growth phase. According to a joint report by the World Economic Forum and McKinsey & Company (2024), the total value of the space economy is projected to expand from approximately $630 billion in 2023 to $1.8 trillion by 2035. This represents a compound annual growth rate (CAGR) of 9%. Over 80% of that value will come from just seven industries, including digital communications, defense, and consumer services. The rise of LEO (Low Earth Orbit) and small satellite constellations is a game-changer—creating a more democratized and software-enabled space economy. As satellites become cheaper to build and launch, their applications multiply across sectors.

The cost of delivering payloads to Low Earth Orbit (LEO) has dropped by multiple orders of magnitude over the past four decades. In 1981, the Space Shuttle program cost nearly $85,000 per kilogram to LEO. Today, with reusable platforms like Falcon 9 and Falcon Heavy, this cost has fallen below $2,000 per kilogram, and future missions aim to push it even lower. Experts forecast that by 2040, space industry will achieve the sub-$100 per kg goal. As launch costs have fallen, the volume of launches has increased more than 2.5x in 10 years, with 254 launches in 2024 alone. Lower CapEx entry points increase the velocity of experimentation and de-risking early-stage bets.

The development and adoption of LEO constellations has been another key enabler. LEO offers significant advantages including Lower latency for communications, smaller, cheaper satellite design, faster time-to-deploy, natural fit for real-time, high-frequency Earth observation.

As the figure illustrates, nearly all of the recent surge in orbital activity is concentrated in LEO, which now dominates global satellite deployments. LEO-focused businesses—from EO data providers to low-latency SatCom players—benefit from shorter development cycles and quicker go-to-market paths.

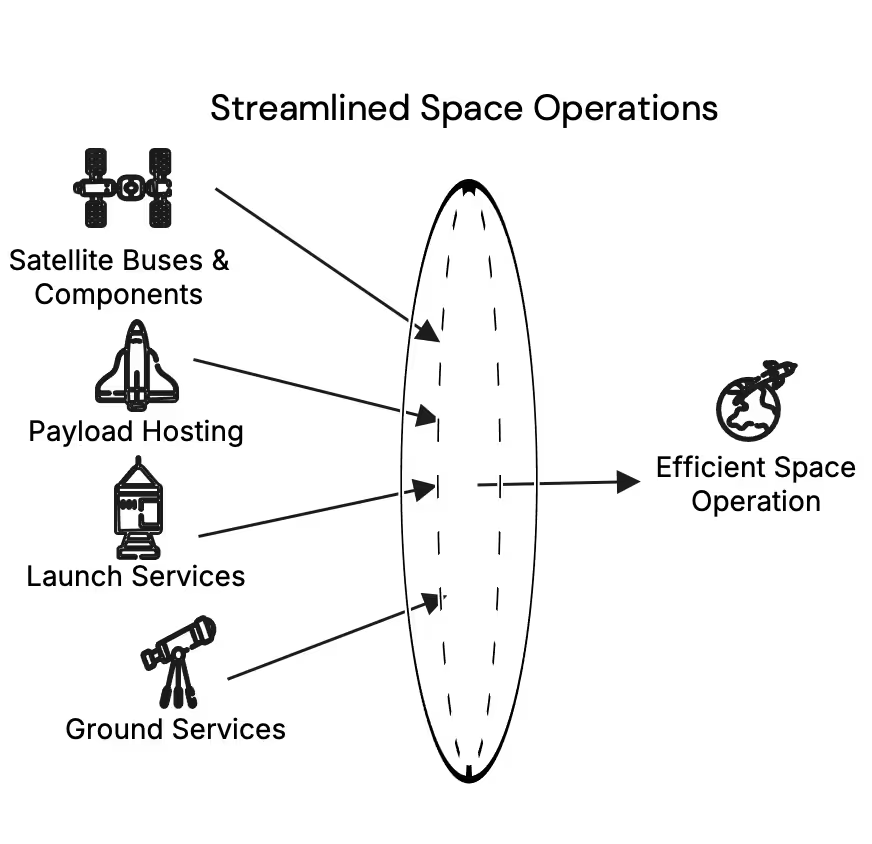

Beyond launches and satellites, the broader space tech stack has become modular and reusable - standardized satellite buses, shared payload hosting platforms, integration-ready launch and ground services

This interoperability has enabled a shift from custom-built missions to stack-based, streamlined operations. Companies no longer need to develop every subsystem in-house; instead, they can plug into an ecosystem that is optimized for efficiency, reliability, and rapid qualification. Modular systems and shared infrastructure drive down time-to-orbit, improve mission flexibility, and increase the likelihood of reaching scale.

This deflationary trend in launch pricing has made space access viable not just for governments or large defense contractors, but for startups, academic missions, and commercial platforms. High launch frequency also means faster iteration cycles for space startups—an essential advantage in early-stage technology development.

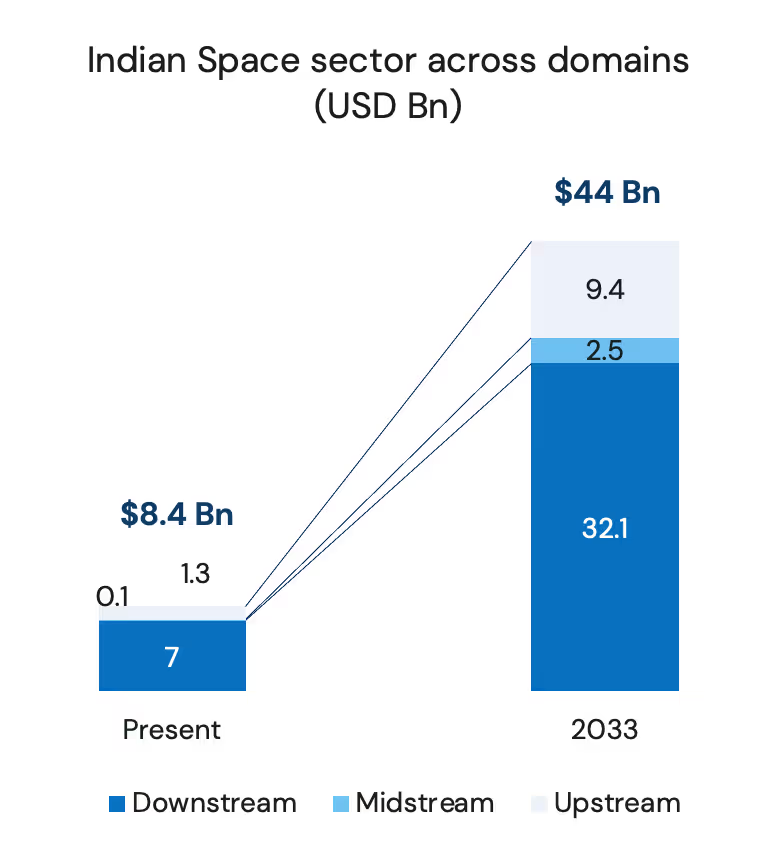

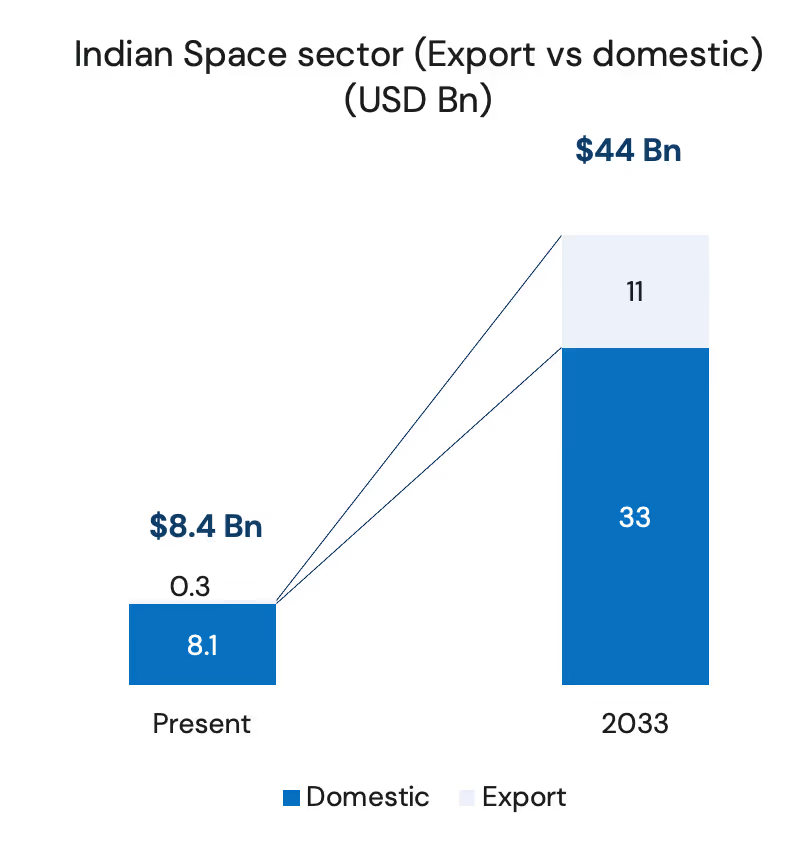

India’s space economy is currently valued at approximately USD 8.4 billion, accounting for around 2% of the global market. While this figure may seem modest, the sector is undergoing a significant transformation. By 2033, India’s space economy is projected to grow more than 5x, reaching USD 44 billion—representing an estimated 8% share of the global space economy.

Today, India’s space revenue is overwhelmingly domestic, with exports contributing only USD 0.3 Bn. By 2033, exports are expected to rise to USD 11 Bn, or 25% of the total space economy. This will be driven by competitive unit economics in launch and manufacturing, growing demand from emerging markets for affordable space-based services and strategic alignment with friendly nations for dual-use technologies.

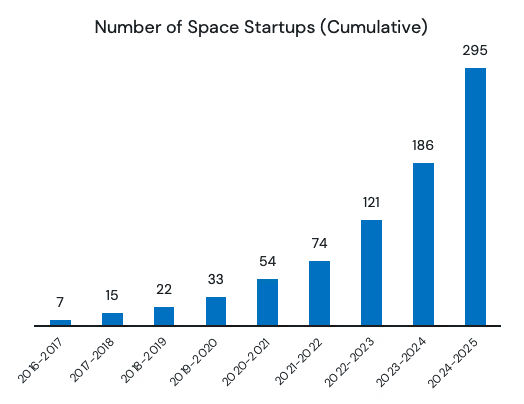

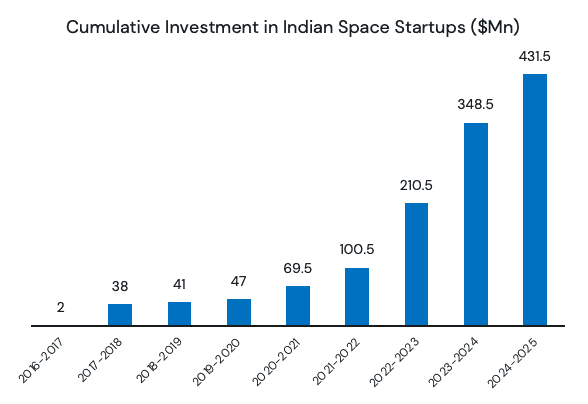

India’s space-tech sector is not only expanding in value—it is also accelerating in terms of entrepreneurship and capital formation. Since the introduction of progressive space sector reforms in 2020, India has witnessed a sharp increase in both the number of startups and the volume of investment in this sector.

As of 2025, Indian space-tech startups have raised USD 430+ million cumulatively.

Over the last four years, the government has built a supportive framework that blends regulatory clarity, commercial access, capital flow, and state-level execution.

The establishment of NewSpace India Ltd (NSIL)—the commercial arm of ISRO—has provided private players with structured access to ISRO’s proven technologies. NSIL acts as a key interface to license technologies, transfer IP, and enable commercial-scale production and launches. NSIL is reducing technical entry barriers and accelerates go-to-orbit timelines for early-stage startups.

IN-SPACe (Indian National Space Promotion and Authorization Center) serves as the single-window clearance and facilitation body for all non-governmental space activities. It oversees licensing, regulatory compliance, safety, spectrum allocation, and coordination with ISRO. IN-SPACe provides the structure needed to de-risk compliance and streamline company formation and launch approvals.

The landmark Indian Space Policy 2023 codified the government's intent to create a commercial, innovation-led space economy. It outlines clear roles for ISRO, IN-SPACe, NSIL, and the private sector. The policy formally integrates private players into national objectives, unlocking dual-use opportunities in both civilian and defense markets.

Under the iDEX program, more than 300 startups have already been engaged to build dual-use and defense-grade space solutions—ranging from micro-propulsion to encrypted satellite communications.

The government now permits 100% Foreign Direct Investment (FDI) in the space sector under the automatic route, eliminating the need for case-by-case approvals. This aligns with India’s broader strategy to position itself as a manufacturing and R&D base for global space firms. Institutional and strategic investors can now participate without procedural delays, improving capital velocity into Indian space ventures.

Indian states such as Karnataka, Gujarat, Tamil Nadu, etc. are now rolling out targeted support for space-tech zones, including dedicated space parks and testing facilities, incentives for R&D and manufacturing and talent development programs.

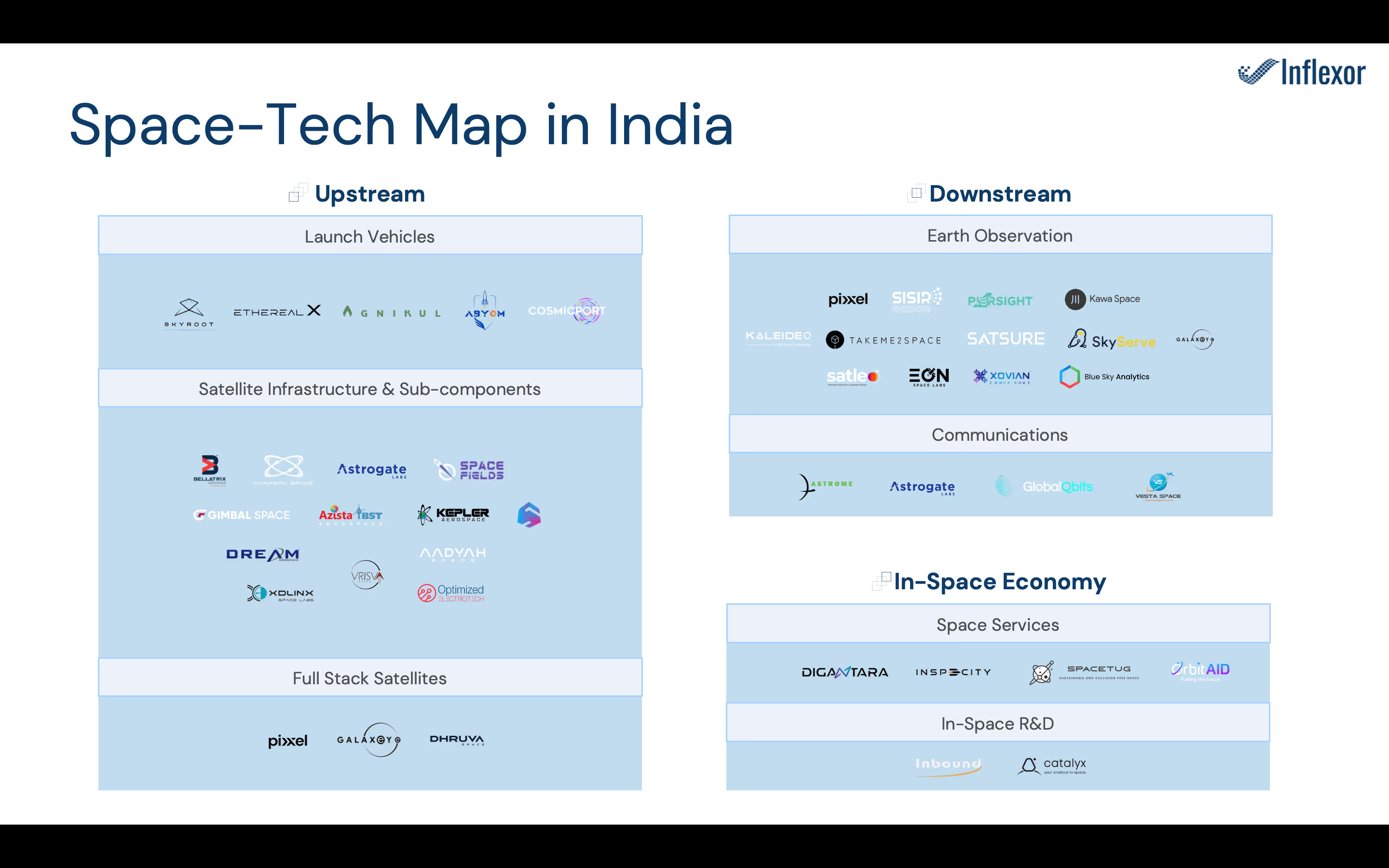

As India’s space-tech sector matures, it is becoming increasingly important to understand how value is distributed across its foundational architecture. We categorize this architecture into three interlinked verticals—Upstream, Downstream, and Auxiliary Infrastructure. Each layer represents not just a stage in the space value chain, but also a distinct investment profile shaped by technology intensity, capital requirements, go-to-market models, and defensibility.

A layered approach to understanding the sector enables investors to identify where innovation is occurring, where value is aggregating, and where capital can be most efficiently deployed.

The upstream layer is the most technically complex and capital-intensive part of the space-tech ecosystem. It is focused on the physical and systemic capabilities that enable humanity to access and operate in space. These companies are essentially building the “hardware layer” of the orbital economy—launch vehicles, satellites, propulsion systems, sub-systems, and mission-critical ground control infrastructure.

The sector is characterised by the below key considerations

The downstream layer comprises ventures that ingest orbital data—derived from satellites, launch systems, and other platforms—and convert it into actionable insights and scalable services. These companies operate closer to the end user. Their strength lies in turning space-derived information into tangible economic outcomes.

The sector is characterised by the below key considerations

Several categories within SpaceTech stand out from an investment lens:

While each theme has a distinct growth curve, they are mutually reinforcing—EO platforms require affordable launch, launchers need orbital safety infrastructure, and connectivity fuels data generation for all other services.

Beyond today’s categories, we anticipate several breakthrough opportunities that could define the next wave of space-tech innovation:

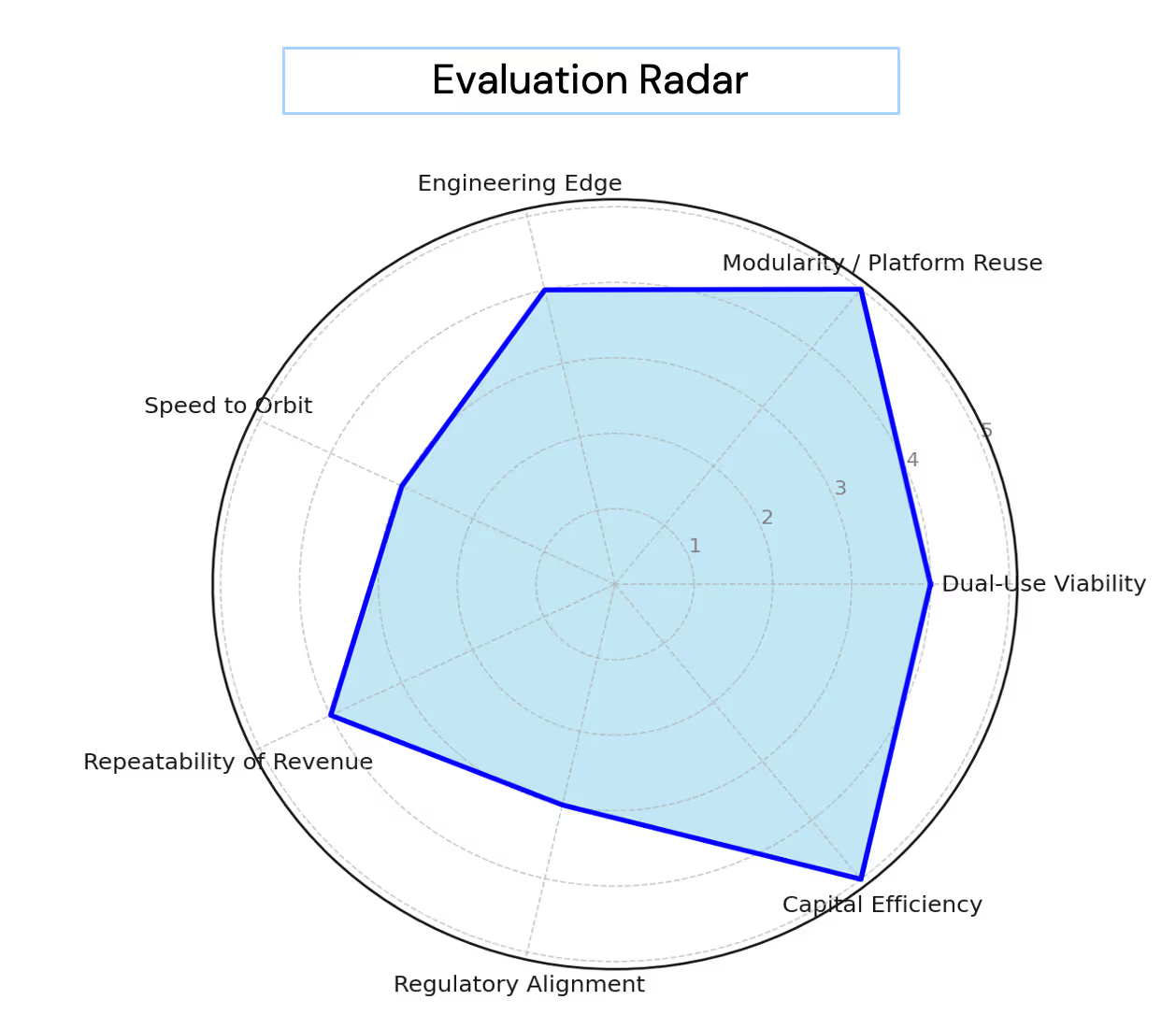

Our approach to space-tech investing is underpinned by a structured evaluation framework designed to balance technical depth, business scalability, and alignment with regulatory policies.

Can the offering serve both civil and defense needs?

Space-tech that enables dual-use applications not only opens larger addressable markets but also aligns with sovereign interests. For example, imaging platforms that support agricultural planning can also fulfill surveillance requirements for defense. This versatility not only enhances addressable markets but also acts as a risk mitigant, ensuring consistent demand across economic cycles.

Dual-use capability also unlocks participation in national security missions, which often come with larger contract values and longer-term engagements. Moreover, companies operating in this space tend to build deeper relationships with government entities, which can support follow-on funding or strategic partnerships.

Can the core technology be reconfigured or reused across missions, customers, or use cases?

Modularity allows startups to amortize R&D across multiple customers, offering tailored solutions without the need for custom-built platforms every time. This is especially critical in a capital-intensive industry like space-tech, where shortening design-to-deployment timelines is key.

Startups with modular architectures are also better positioned to participate in multiple value pools—ranging from national launches to commercial payloads—without a complete redesign. Additionally, modularity contributes to faster product iteration cycles and smoother integration into customer ecosystems.

Is there deep technical differentiation in propulsion, materials, electronics, or avionics?

IP-rich innovation is a critical defensibility layer and a lever for licensing, export, or acquisition pathways. Favor engineering-first companies that can build moats through proprietary design or process innovation.

How fast can the team go from design → build → test → launch?

Time-to-orbit is increasingly becoming a strategic advantage. Startups that can reduce lead times, iterate rapidly, and adapt to customer needs faster are better positioned to win early market share. This speed reflects organizational agility and manufacturing maturity.

We assess not just hardware development pace, but also the team’s ability to navigate test regimes, regulatory clearances, and launch coordination. Companies with in-house or local prototyping capabilities, as well as experience with rapid validation frameworks, tend to outperform in this metric.

Does the business model lend itself to recurring or repeat contracts?

We look for business models that are not purely transactional but exhibit elements of stickiness and predictability. This includes satellite data services sold on a subscription basis, recurring launch partnerships, or software platforms layered on space assets.

Repeatability indicates customer satisfaction, reduces volatility, and creates stable revenue baselines. It also improves valuation multiples over time. Even for hardware-first startups, building adjacent services or offering maintenance contracts can significantly enhance revenue quality.

Is the company actively engaging with IN-SPACe, NSIL, or other statutory authorities?

Navigating India's evolving space policy framework is essential for success. Engagement with ISRO, NSIL, IN-SPACe, and iDEX is not just a checkmark—it’s an enabler of credibility, risk reduction, and scale.

Is the startup achieving key milestones with lean capital or government leverage

We look closely at how efficiently startups utilize their capital. Those who demonstrate significant technical progress—such as launch-readiness, working prototypes, or paying pilots—without excessive burn are more attractive investment targets. Efficiency is especially important in upstream segments where costs can escalate rapidly.

Startups that actively co-leverage government R&D infrastructure, utilize grants effectively, or tap into university partnerships often gain more runway for the same investment. Capital-efficient teams also tend to be more disciplined with go-to-market strategies, enabling better long-term capital planning.

This framework helps us evaluate defensibility, capital fit, and long-term scalability across the SpaceTech stack.

India is not just catching up—it’s setting up to lead. With policy support, rising talent, and an increasingly global customer base, Indian SpaceTech is ready to take off. The next decade will see new constellations, strategic collaborations, and potentially, category-defining outcomes.

For founders, it’s an opportunity to build infrastructure for Earth from space. For investors, it’s a moment to back high-IP, globally exportable, and mission-aligned technologies.

We’re just getting started.

If you are working on an ambitious startup in space technology, we'd love to connect. Reach out to us at team@inflexor.vc or drop us a message on LinkedIn - let's explore how we can help you go further, faster.