In 1920, the factory's most sophisticated sensor was a man. A veteran machinist who could hear a bearing fail before it happened, feel misalignment through a handshake with a machine, and smell trouble in the air. He was irreplaceable. And that was exactly the problem.

Now picture a comparable plant today. Ten thousand sensors stream real-time temperature, vibration, and torque data from every machine. An AI model trained on years of operating history predicts bearing failure seven days in advance. A cobot on the adjacent line has just been reprogrammed via tablet to run a new component specification. The factory’s intelligence is no longer locked inside human experience. It is embedded in the walls, the machines, the software, the data.

That transition from intelligence as a human trait to intelligence as a structural property of physical infrastructure, is what this thesis is about.

💡 The industrial economy is not becoming a software business. It is becoming an intelligence business. We are at the beginning of a multi-decade structural transformation, and the venture window, the moment when category leaders are still being created rather than consolidated, is open right now.

This piece lays out the full thesis: what the Intelligence Layer is, why it is happening now, where the largest opportunities sit, what we look for in companies, and what the risks look like honestly assessed.

The industrial world has been through four distinct revolutions. Each revolution was enormous. But none of them moved intelligence from humans to systems in any deep way. The factory might be connected in Industry 4.0, but the decisions - when to reorder raw materials, how to schedule maintenance, how to re-route logistics around a disruption, still required a human expert to interpret the data and act on it.

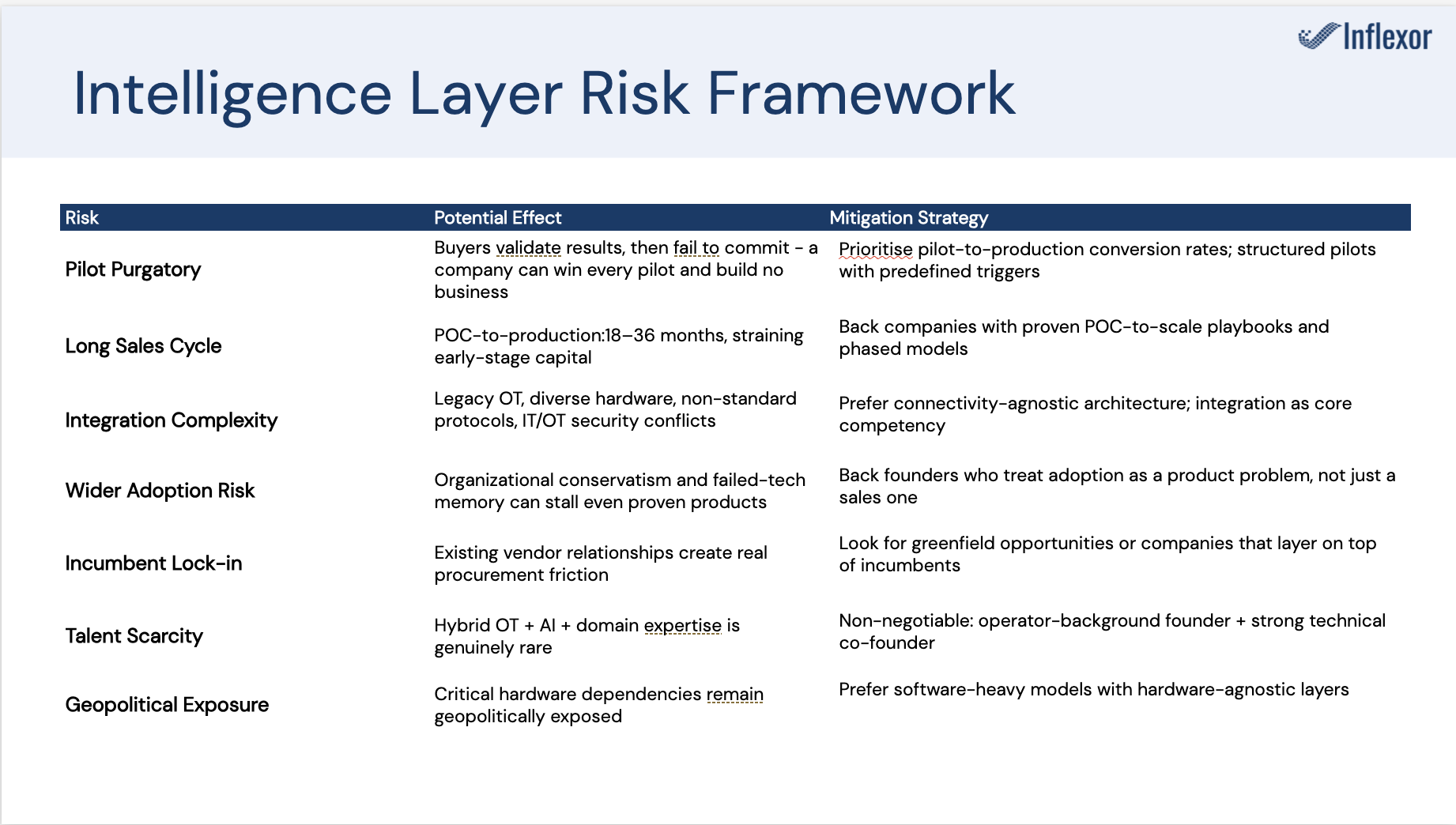

Several structural barriers explain why:

These barriers created a 30-year lag between the software revolution in digital industries and its arrival in physical ones. That lag is now ending.

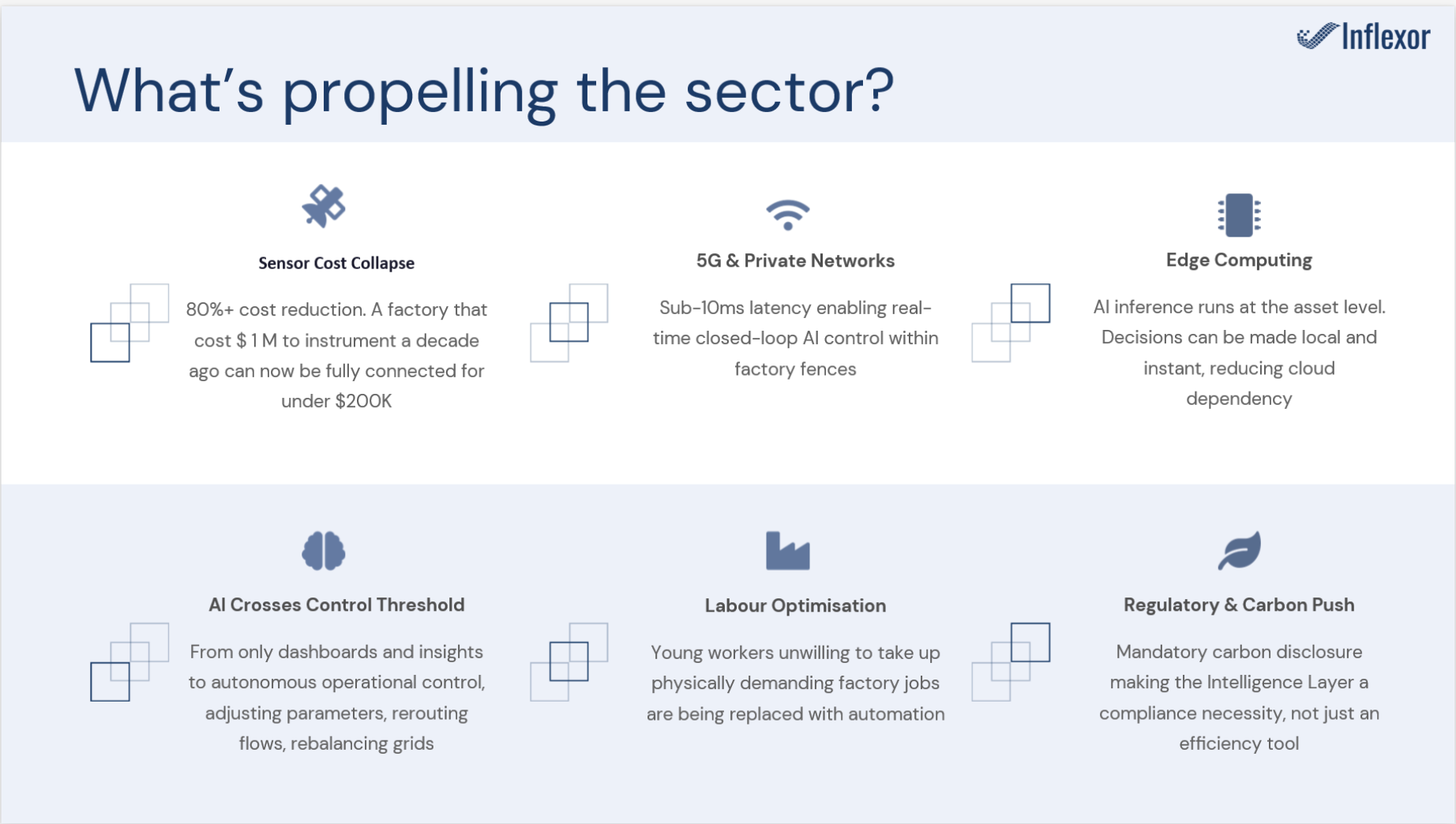

For the better part of three decades, the Intelligence Layer was a thesis in search of infrastructure. The ambition was clear; the enabling conditions were not. Each prior wave of industrial technology investment stalled because one or more foundational requirements remained unmet. What has changed is not the ambition, it is the infrastructure. Six enabling conditions have now reached the maturity threshold required for large-scale deployment, and for the first time, all five are present simultaneously.

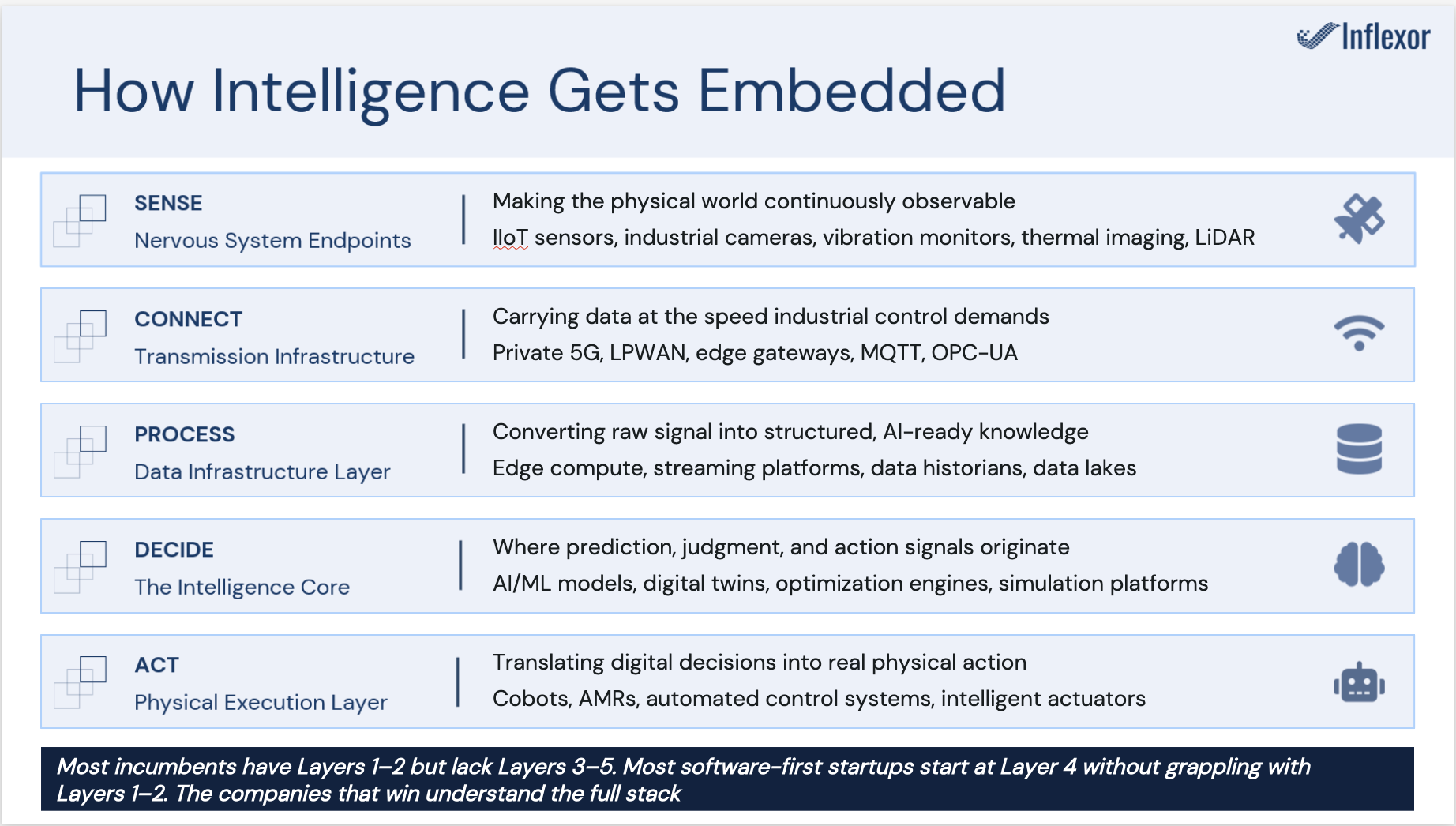

The architecture of the intelligence layer can be modeled as a 5-layer stack that mirrors the human biological system: Sensing, Transport, Data, Intelligence, and Action.

The companies that will win are those that understand the full stack, or partner intelligently across it.

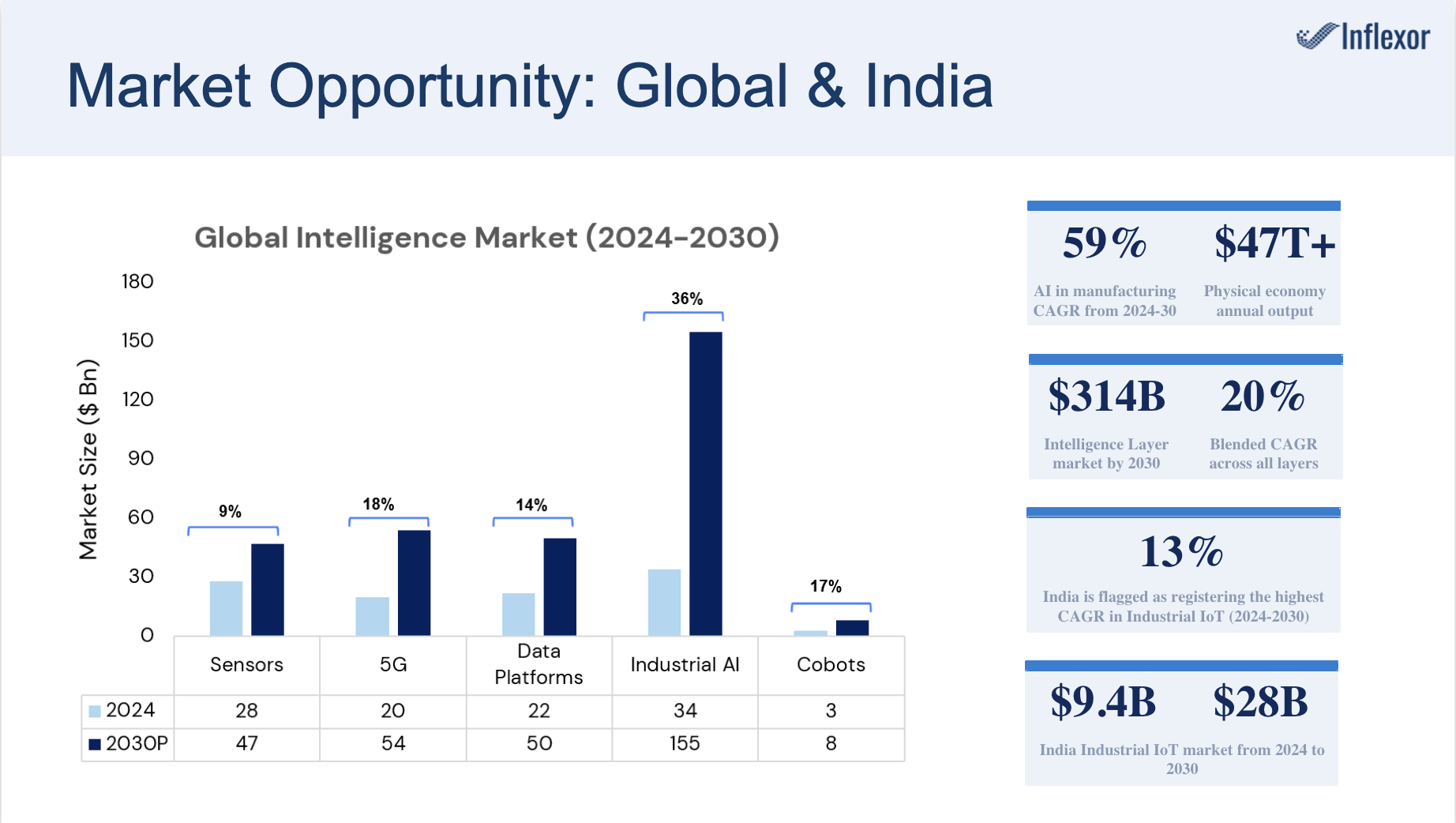

The transition of physical industries from human-reliant operations to AI-driven ecosystems represents one of the largest capital reallocation events in history. We are looking at a market shift defined by macro tailwinds, including structural labor shortages, volatile global supply chains, and sweeping decarbonisation mandates.

The market for Intelligence Layer technology spans several overlapping but distinct categories: the hardware and connectivity infrastructure that generates and transmits industrial data (IIoT), the AI software and platforms that reason over that data, and the robotic and automation systems that execute on those decisions. Across all three dimensions, the numbers point to the opportunity.

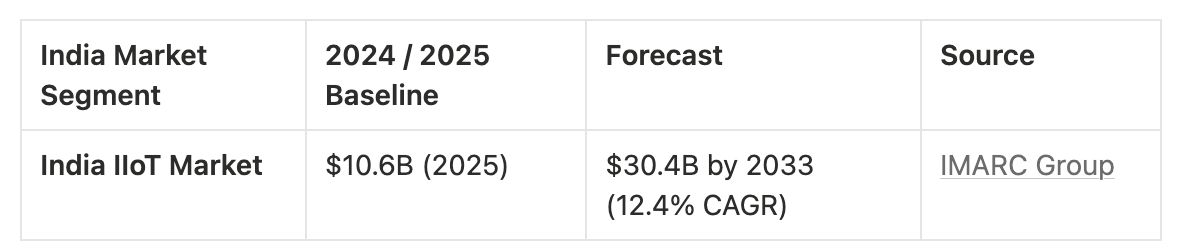

India occupies a structurally unique position in the Intelligence Layer thesis. It is simultaneously a massive end-market for industrial automation, a growing source of deep-tech industrial AI companies, and the world's preferred destination for global manufacturing re-shoring. The combination of all three creates a compounding opportunity that is difficult to find elsewhere.

Notably, India is flagged as registering the highest CAGR in Industrial IoT during the forecast period among all major economies according to MarketsandMarkets-a distinction that reflects the structural catch-up underway as India's manufacturing sector modernises from a low base at speed. The AI in manufacturing segment is growing at a particularly steep 58.96% CAGR through 2028, making it one of the fastest-accelerating industrial intelligence markets globally.

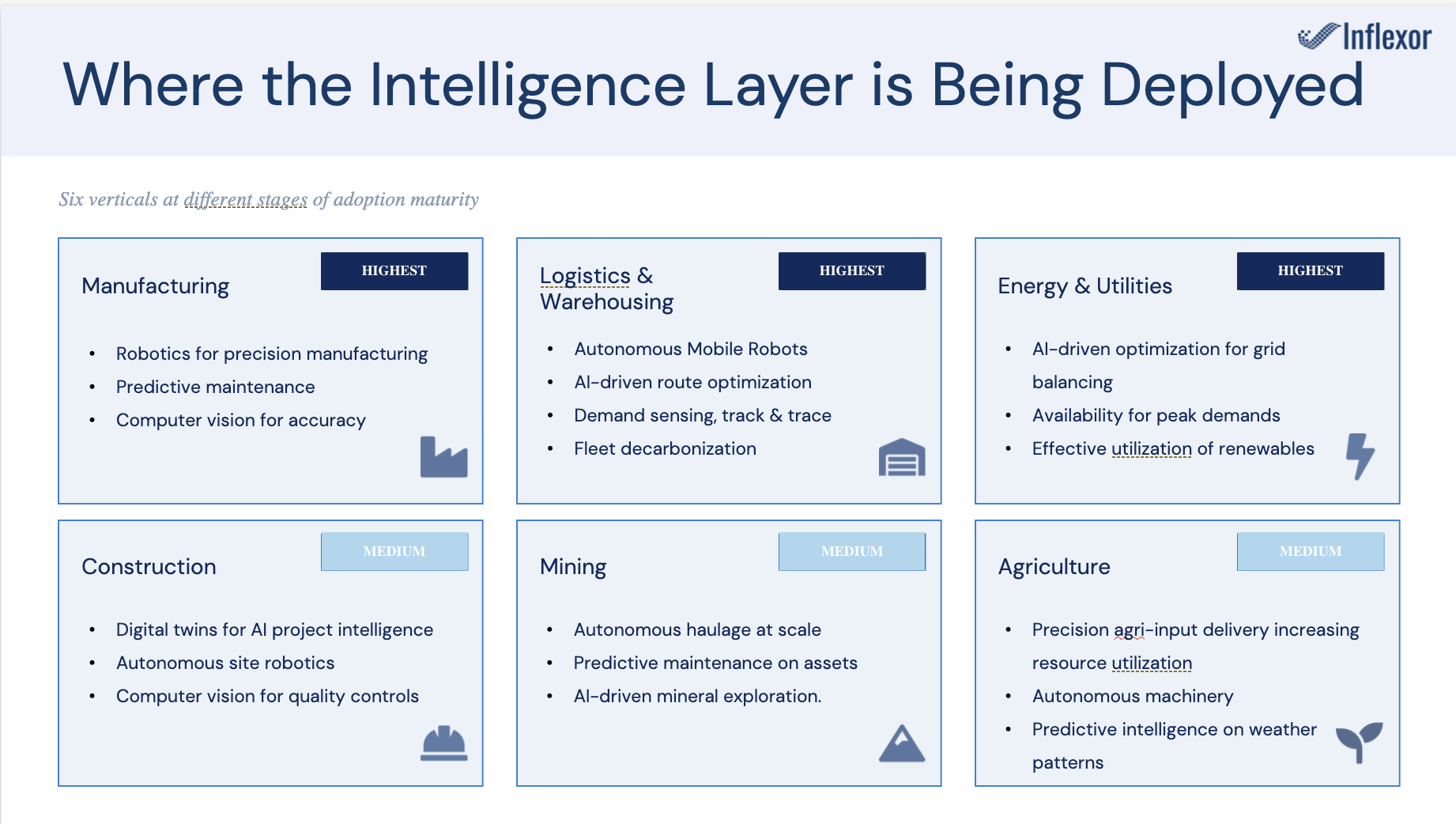

The deployment of the intelligence layer is already reshaping traditional industries, with specific use-cases demonstrating significant ROI.

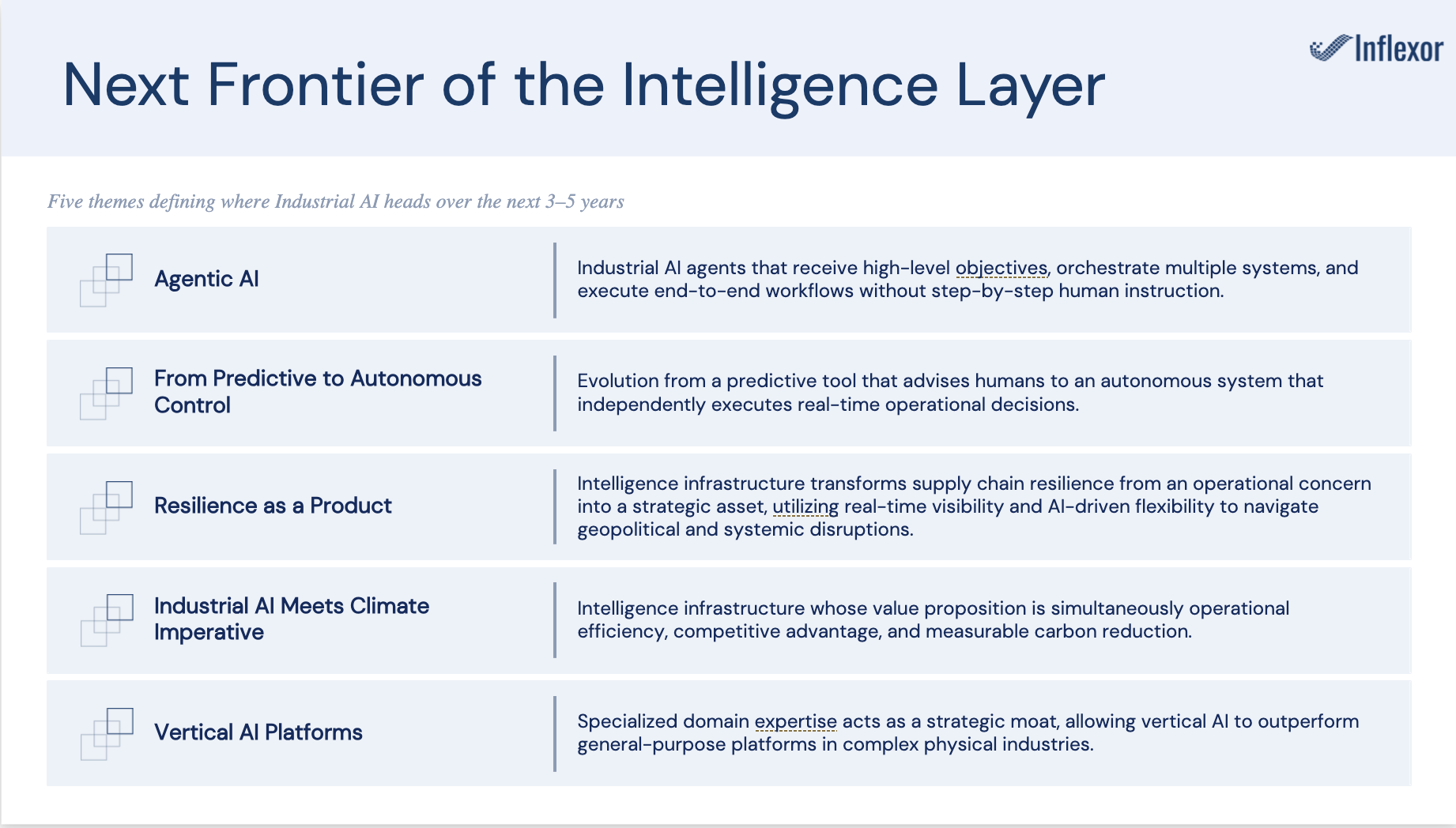

The foundational deployment wave of the intelligence layer - instrumenting assets, connecting infrastructure, and applying AI to the most obvious use cases, is already underway. What comes next is a second wave of deeper, more autonomous, and more structurally consequential capability. Following trends define where the Intelligence Layer is heading over the next 5 years.

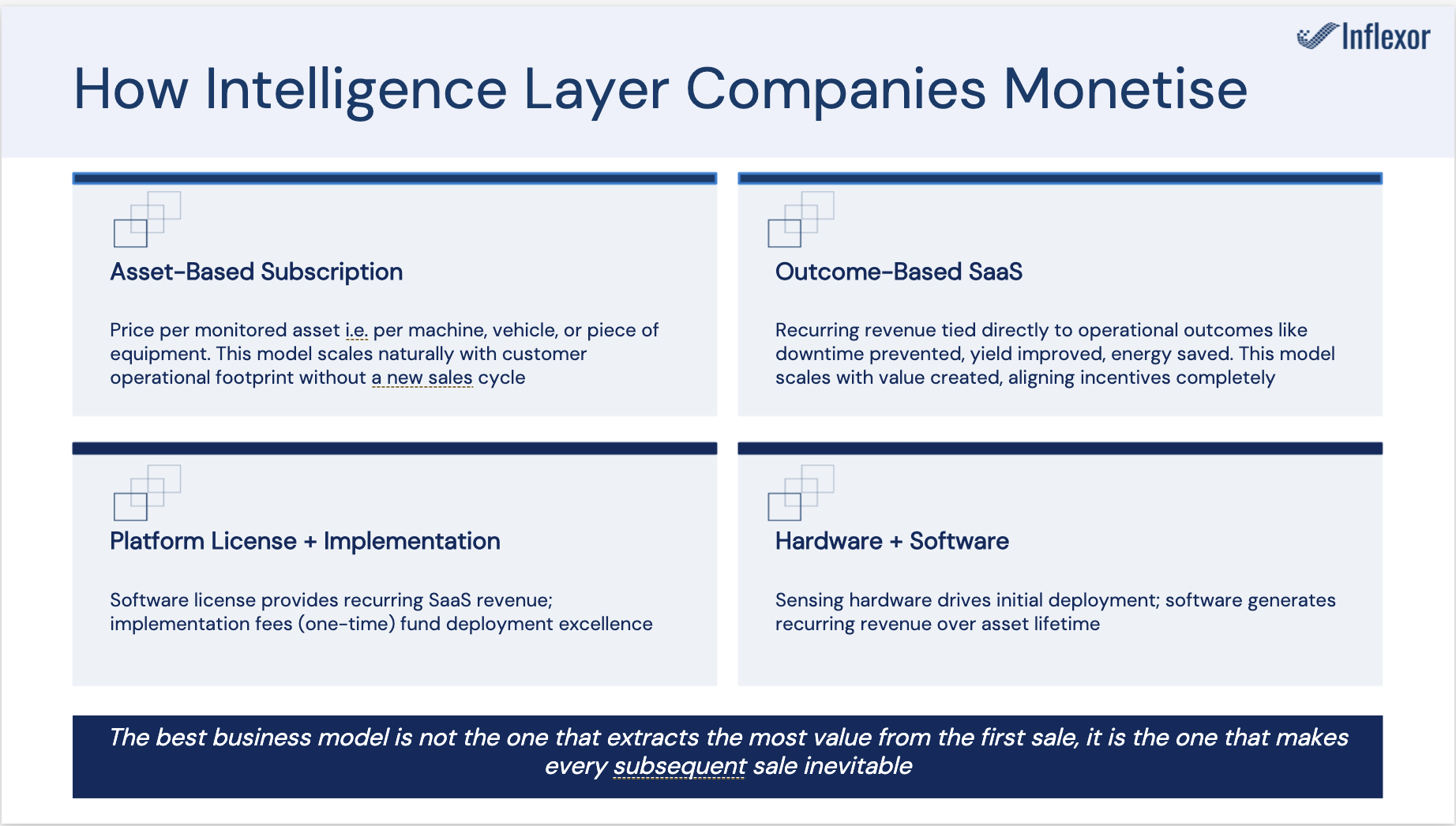

No single revenue model is universally superior in the Intelligence Layer, the right model is determined by where a company sits in the stack, the maturity of its deployment base, and the measurability of the outcomes it delivers. The most durable industrial AI companies are moving toward outcome-based and asset-linked pricing models that scale naturally with customer success and align vendor incentives directly with operational results. The best business model in the Intelligence Layer is not the one that extracts the most value from the first sale, it is the one that makes every subsequent sale inevitable.

The intelligence layer is the ultimate orchestrator of the industrial economy. The shift from intelligence residing in human experience to intelligence embedded in physical infrastructure is not a technology story. It is an economic story about where value is created, captured, and compounded across the largest industries in the global economy.

We are moving toward a state of "Autonomous Infrastructure" where factories, ports, and grids do not just monitor themselves but self-correct and optimize in real time through Agentic AI. The intelligence layer is no longer a peripheral software enhancement; it is the fundamental infrastructure upon which the future physical economy will be built.

For decades, the intelligence of physical industries lived inside human experience, the veteran machinist who could hear a bearing fail, the logistics manager who knew which supplier to call. That era is ending. Inflexor's latest thesis, The Physical Intelligence Stack: Architecture for the Modern Economy, makes the case that software, data, and AI are now embedding a digital nervous system into the world's most asset-heavy industries like manufacturing, logistics, energy, and infrastructure, and that this transition represents one of the defining investment opportunities of the next decade. The thesis maps the full architecture of this shift, from sensing and connectivity at the edge to AI reasoning and autonomous action at the top of the stack, identifies where the largest opportunities sit across global and Indian markets, and lays out the criteria Inflexor will apply in backing the companies that will define this category. We are at the beginning of a multi-decade structural transformation, and the window to back category leaders before consolidation sets in is open right now.