There's a coin flip game I want you to try mentally.

Heads: your investment goes up 50%. Tails: it drops 40%. The coin is fair. You can play as many times as you want.

Go ahead — should you play?

Most people say yes. The expected value is +5% per flip. Positive edge. Take the bet.

But if you actually played this game 100 times, you'd almost certainly go broke. The median player ends up with a fraction of what they started with — even as the average looks great on paper, propped up by a handful of people who happened to flip heads early and often.

This isn't a trick. It's one of the most underappreciated ideas in finance. And I think it quietly reshapes every decision in venture — whether or not we have a name for it.

This is called non-ergodicity. A process is ergodic if the average across many parallel universes equals the average of one person across time. For most financial processes — especially multiplicative ones like investing — these two are not the same.

The distinction matters because expected value is an ensemble calculation. It asks: “If a thousand parallel versions of me made this bet simultaneously, what would they average?” That’s not the question you’re actually facing. You get one path through time. Not a thousand.

So when you’re evaluating a deal and asking “what’s the expected return?”, you may be solving the wrong problem. The better question is: “What does this bet do to my fund’s geometric growth rate over time?”

Most financial models assume you live in all possible worlds at once. You don’t.

The math is simple but brutal. When returns are additive — you win or lose a fixed dollar amount — ensemble and time averages coincide. The law of large numbers applies cleanly. But when returns are multiplicative — you win or lose a percentage of current wealth — the two diverge sharply. Losing 40% requires a 67% gain just to break even. The asymmetry compounds with every step.

VC returns are purely multiplicative. A company goes to zero or returns 50x on capital deployed — not on some fixed notional. This is why standard expected-value thinking can quietly mislead even experienced GPs.

Every layer of the VC structure is solving a different non-ergodicity problem. Misreading which problem the other party is solving is the source of most structural misalignment in venture — not bad intent, not misaligned incentives in the classic sense. Just different positions on the ergodicity spectrum.

The LP has diversified across GPs, strategies, and vintages. They’re closest to ergodic — their ensemble average and time average begin to converge. They can absorb J-curves, write-offs, and long lock-ups without existential concern. Their game is the long-run geometric growth of total AUM.

The GP sits in the middle. With 20–30 bets in a fund, there’s some diversification. But carry is path-dependent. Reputation compounds or decays over fund generations. They’re diversified within a fund, but serially exposed across them.

The founder is maximally non-ergodic. One company. One path. No averaging across alternatives. Their entire career capital, and often personal savings, rides a single multiplicative bet. Their wealth trajectory either compounds or collapses — there is no parallel-universe outcome to smooth things out.

The GP is solving an ensemble problem: what does this distribution of outcomes do for my fund? The founder is solving a time-path problem: what happens to me? They are literally playing different games — at the same table.

This shows up in practice more often than we admit:

Neither is wrong. They’re just not playing the same game.

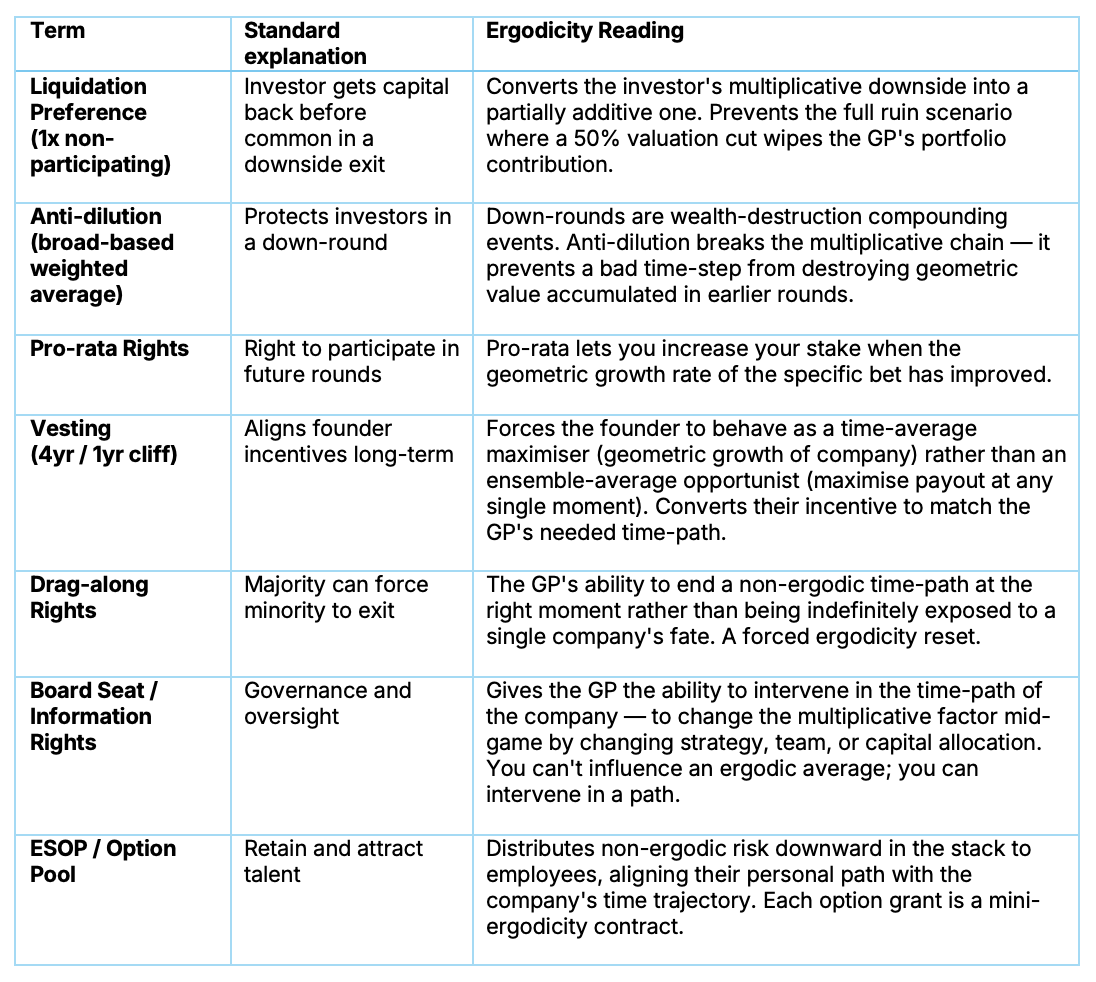

Standard VC deal terms are not just legal protections — they are ergodicity corrections. Every major clause is, at its core, a mechanism for redistributing non-ergodic risk between agents at different layers of the stack. Once you see it this way, term negotiations look different.

Every negotiation over deal terms is, in essence, a negotiation over who absorbs the non-ergodic risk at each layer. The GP wants to offload as much multiplicative downside as possible onto the structure — through preferences and anti-dilution — while retaining upside exposure through pro-rata and participation rights.

The follow-on question — how much to reserve for which portfolio companies, and when — is the most consequential ongoing ergodicity decision a GP makes. And most funds don’t have a rigorous framework for it.

A company that has materially de-risked — found PMF, strong cohort data, clear path to the next milestone — has a higher geometric growth rate on that path than it did at initial investment. The Kelly-rational response is to increase your stake. This is the mathematical basis for pro-rata rights, and why top-tier GPs fight hard for them.

Conversely, averaging down into a struggling company — the sunk-cost follow-on — is an ergodicity error. The geometric growth rate of that path has declined. Deploying more capital into it reduces, not improves, the fund’s overall compounding.

Most GPs make follow-on decisions based on gut, relationship, and conviction. Ergodicity gives you a cleaner question: has the geometric growth rate of this path improved since my last check? If yes, lean in. If not, hold.

There’s a formula called the Kelly Criterion — used by professional gamblers and a handful of quant funds — that calculates the exact portfolio allocation that maximises geometric growth rather than expected value. Most experienced GPs approximate it intuitively. It’s why “never put more than 8–10% of the fund in a single name” is common wisdom. The math actually supports that range precisely.

In practice, it means follow-on decisions should be driven by whether a company’s geometric growth rate has improved.

The next time someone pitches you a deal with strong expected returns, the most important follow-up isn’t “what’s the downside scenario?” It’s: “What does this bet do to the path I’m actually on?”

Those are different questions. And in venture, the path is all you get.